In the face of planetary crises, from biodiversity collapse to freshwater scarcity, business as usual is no longer sustainable. A key reason is that many environmental systems function within ecological thresholds, or tipping points, beyond which damage becomes irreversible or exponentially worse. These thresholds are central to understanding both risk and responsibility. Under the EU’s Corporate Sustainability Reporting Directive (CSRD), companies are now required to measure and report against them.

What you will learn

✅ What ecological thresholds are, and why they matter for sustainability disclosures

✅ How CSRD and the European Sustainability Reporting Standards (ESRS) reference ecological limits

✅ How companies can operationalize thresholds using tools like SBTN’s science-based targets

✅ Why thresholds are essential for assessing double materiality

By the end, you’ll understand why aligning with ecological thresholds is beneficial.

2. What are ecological thresholds?

Ecological thresholds mark the points at which a small additional impact can cause a disproportionate, often abrupt, shift in an ecosystem’s structure or function. For example:

A wetland may absorb pollutants until a threshold is crossed, beyond which it can no longer purify water.

A forest may maintain biodiversity until cumulative land-use change disrupts its regeneration capacity.

These thresholds define what is safe and just for nature and society. Operating within them is critical to maintaining Earth’s life-support systems.

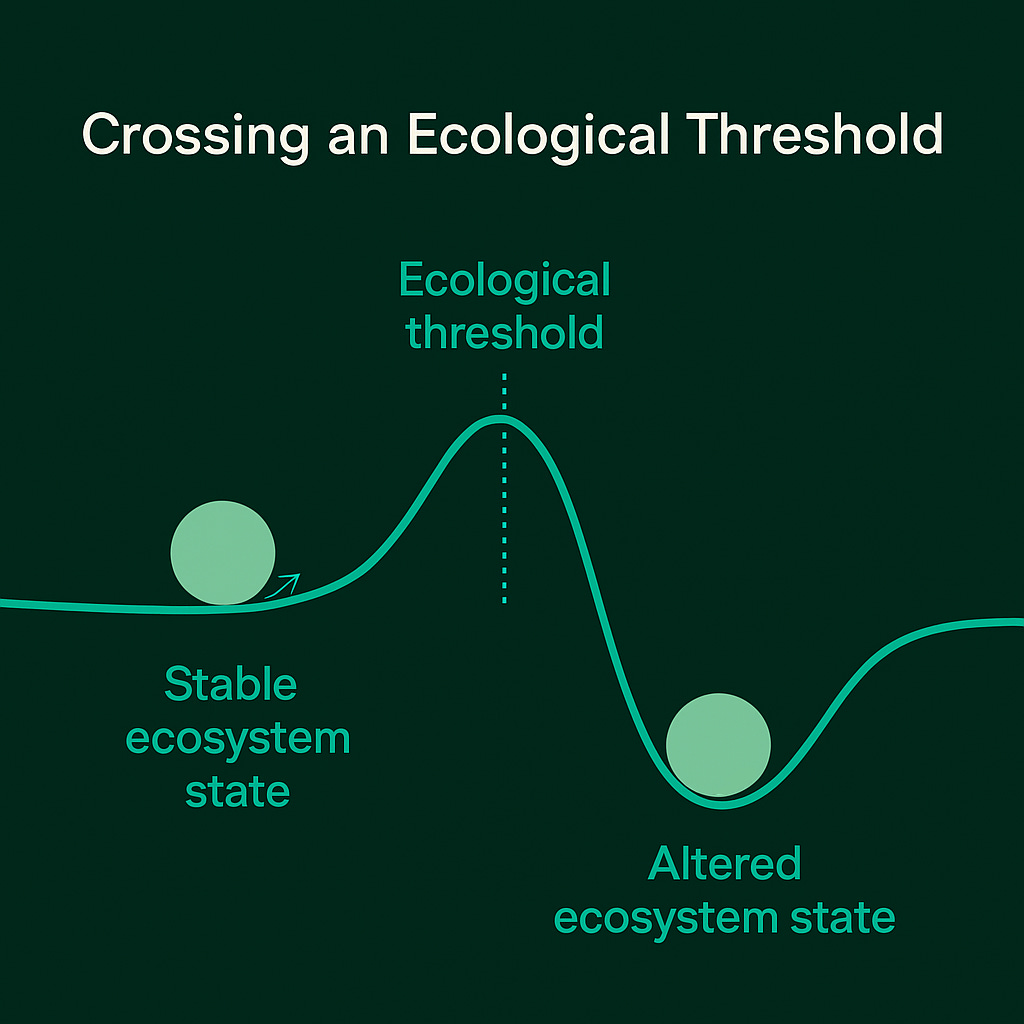

This diagram illustrates how ecosystems can shift between stable states when ecological thresholds are crossed. The ball represents the system; the curve represents ecosystem stability. As pressures increase, the system moves toward a tipping point—the ecological threshold—marked at the peak. Once crossed, the system transitions into a new, often degraded state, which can be difficult or impossible to reverse. Understanding where these thresholds lie is critical for setting sustainability targets that truly protect ecosystem integrity.

3. How the CSRD integrates ecological thresholds

The CSRD and its European Sustainability Reporting Standards (ESRS) refer to ecological thresholds as operational criteria for setting science-based targets and evaluating corporate impacts.

ESRS E2 – Pollution

In ESRS E2, undertakings are encouraged to state whether and how ecological thresholds—such as biosphere integrity, ocean acidification, and atmospheric aerosol loading—were considered when setting pollution-related targets (E2-3). This includes describing:

The thresholds identified and methods used

Whether thresholds are entity-specific

Allocation of responsibility for respecting them

ESRS E3 – Water and marine resources

ESRS E3-3 requires disclosure of water-related targets and explicitly allows undertakings to report whether those targets are based on ecological thresholds and entity-specific allocations (para. 24). It further references the Science-Based Targets Network (SBTN) as a scientifically grounded methodology for identifying such thresholds (AR 22). Companies may also disclose:

Whether thresholds are local, national, or global

How they relate to areas at water risk or high water stress

How responsibility for respecting them is distributed internally

ESRS E4 – Biodiversity and ecosystems

Here, the language is explicit and mandatory. Under Disclosure Requirement E4-4, companies must report:

Whether ecological thresholds and allocations of impacts were applied when setting biodiversity targets

The thresholds identified and their methodologies

How responsibility for those thresholds is distributed across the organisation

ESRS E5 – Resource use and circular economy

ESRS E5-3 allows companies to refer to ecological thresholds to justify circular economy targets and explicitly cites the Science-Based Targets Network (SBTN) as a source of scientifically acknowledged methodologies. These thresholds may be local, national, or global.

4. SBTN: A pathway to operationalize thresholds

The Science-Based Targets Network (SBTN) defines ecological thresholds as the biophysical limits required to maintain Earth system stability and function . Its approach offers businesses a methodical way to respect these boundaries:

Step 3 of SBTN (“Measure, Set & Disclose”) requires companies to align their targets with scientific thresholds—e.g., maximum safe levels of nutrient runoff or permissible land-use change.

These thresholds are context-specific: what’s sustainable in one location may not be in another. That’s why SBTN emphasizes location-based baselines and targets .

The concept of thresholds informs SBTN’s ambition-setting—companies must go beyond incremental improvements and align their activities with what science says ecosystems can tolerate.

This threshold-based method matches the spirit and structure of the CSRD. Where CSRD asks for targets “in line with policy goals and scientific consensus” (ESRS E4-4), SBTN provides the means to deliver.

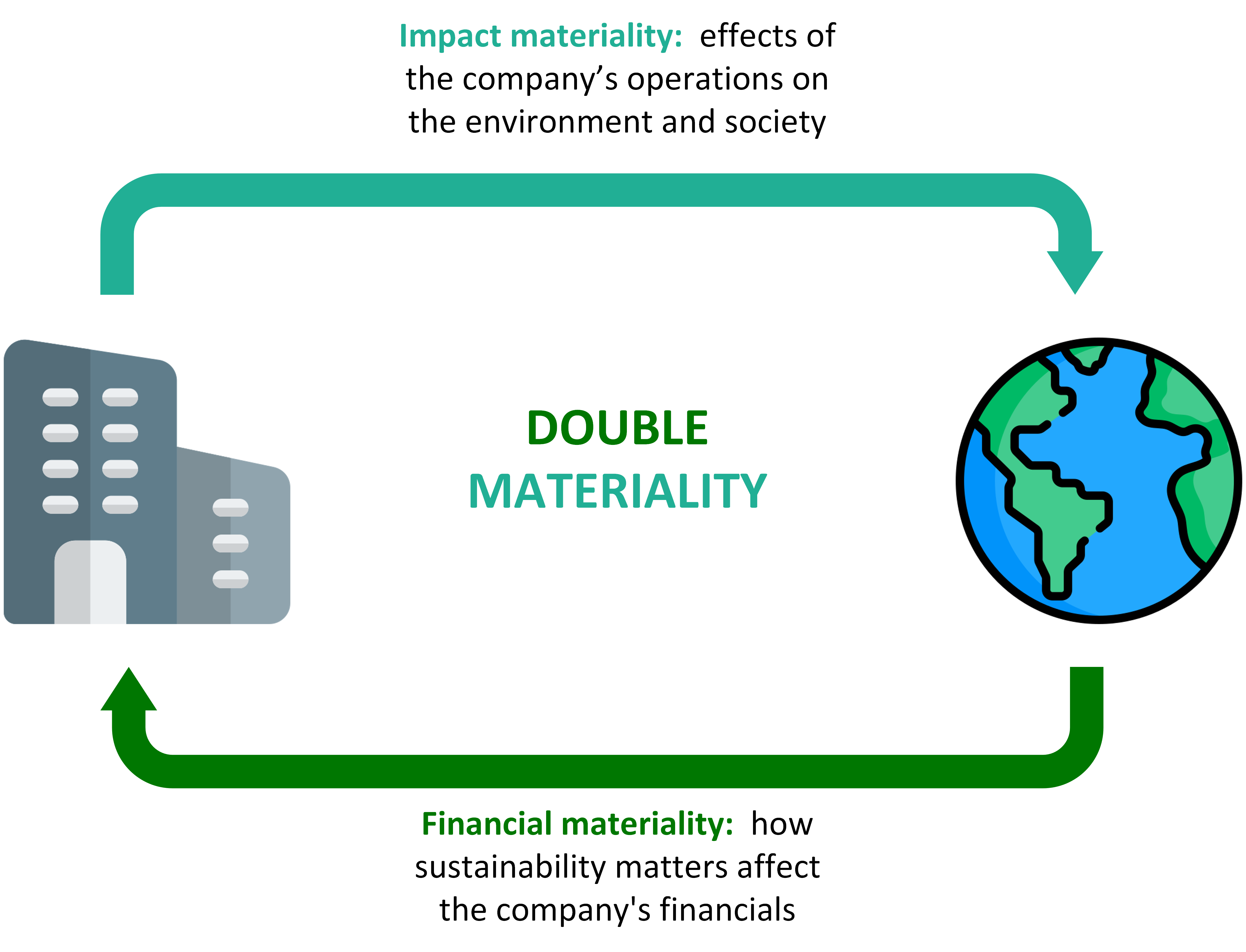

Under the CSRD, companies must identify material sustainability matters through a double lens: impact and financial materiality.

Ecological thresholds play a pivotal role in both:

Impact materiality: A company’s operations might push a watershed beyond its nitrogen threshold, harming aquatic biodiversity—a clear negative impact.

Financial materiality: That same threshold breach could expose the company to legal penalties, reputational damage, or resource shortages.

Thus, understanding and respecting thresholds helps companies better define materiality, avoid greenwashing, and prepare for scrutiny by auditors and stakeholders.

Check out this article to learn how to perform a materiality assessment:

If your company is preparing for CSRD-aligned disclosures, ecological thresholds can be very important and usefull. Here’s how to move forward:

1. Start integrating thresholds now Begin by mapping where your company’s operations intersect with environmental thresholds. Prioritize geographies and activities most likely to exceed safe limits, whether it’s nitrogen pollution, freshwater withdrawals, or habitat loss.

2. Use the SBTN framework as a practical entry point The Science-Based Targets Network provides step-by-step guidance for assessing impacts, setting context-specific thresholds, and disclosing targets. Start with available tools and data to align your efforts with scientifically credible boundaries.

3. Strengthen internal capacity and governance Threshold-based disclosure demands collaboration across sustainability, risk, operations, and finance teams. Establish cross-functional working groups and ensure leadership understands the strategic implications of operating within ecological limits.

4. Prepare for deeper disclosure and third-party scrutiny The CSRD will drive more granular, auditable data demands. Build data systems that can localize impacts and track performance relative to ecological ceilings.

By taking these steps, your company will build resilience.

Thanks for reading CSRD Simplified! This post is public so feel free to share it.