[BREAKDOWN] E1-8: Choosing operational boundaries for emissions reporting

ESRS E1: How do you choose operational boundaries for emissions reporting? Using the GHG protocol.

Last updated: 08-08-2025

1. Introduction

When businesses report their greenhouse gas (GHG) emissions, defining operational boundaries is just as important as knowing which entities to include. Operational boundaries determine what types of emissions a company must report.

Setting these boundaries helps companies understand where their emissions come from, which sources they can control or influence, and how to prioritize reduction efforts, all while ensuring compliance with frameworks like the GHG Protocol and CSRD.

This article will help you understand:

✅ The three types of emission scopes and how they differ

✅ How to map and prioritize your company’s emission sources

✅ What to include or exclude in Scope 3 reporting and how to justify it

✅ A step-by-step guide to setting operational boundaries

✅ What the CSRD (ESRS E1) requires for reporting Scopes 1, 2, and 3

By the end of this article, you’ll know how to set operational boundaries that are complete, consistent, and aligned with regulatory expectations.

2. Understanding organizational vs. operational boundaries in GHG accounting

See this article for more information about organizational boundaries.

![[EXPLAINED] E1-8: What are organizational & operational boundaries for emissions reporting?](https://substackcdn.com/image/fetch/$s_!rTGI!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F20657086-78d5-4c2d-948b-8af47f39625e_2048x2048.jpeg)

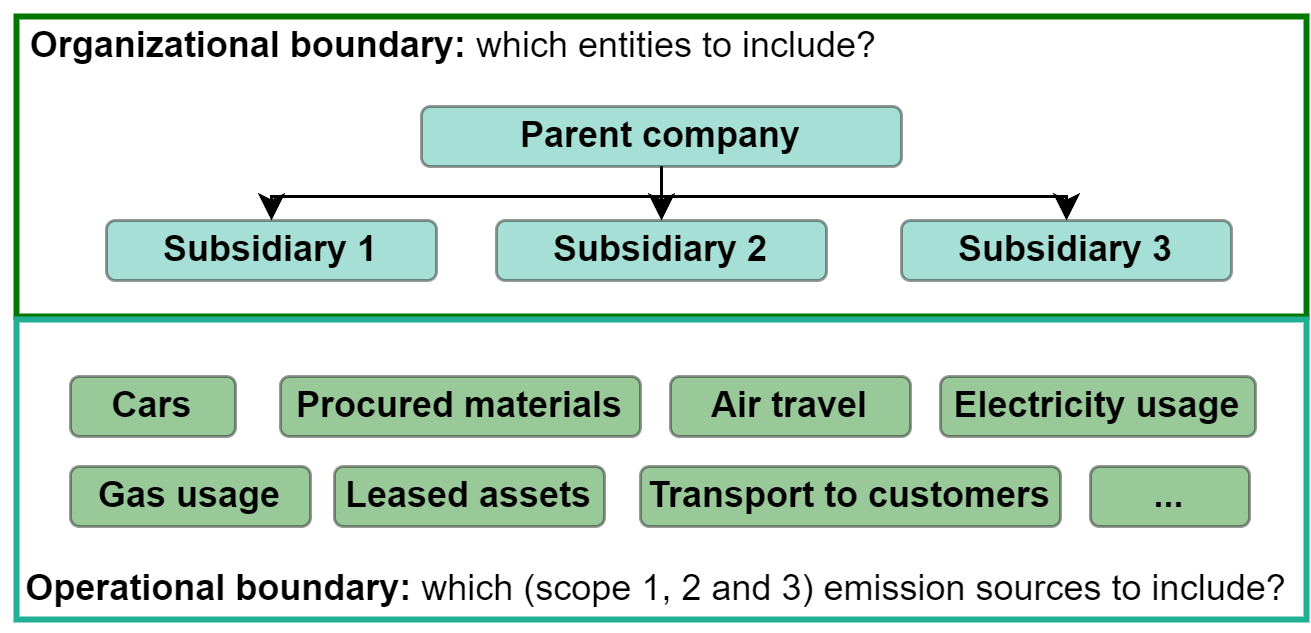

Operational boundaries: what activities produce emissions?

Once you’ve defined who is included (organizational boundaries), you need to figure out which emissions to track (operational boundaries). These are categorized into three scopes:

Once a company has established its organizational boundaries, determining which entities or subsidiaries are included in emissions reporting, the next step is setting operational boundaries. This means categorizing emissions into three key scopes and setting boundaries:

Scope 1 (direct emissions) – From sources your company owns or controls (e.g., company vehicles, on-site fuel combustion).

Scope 2 (indirect emissions from energy) – From purchased electricity, steam, or heating/cooling.

Scope 3 (other indirect emissions) – All other indirect emissions (e.g., business travel, supply chain, waste disposal).

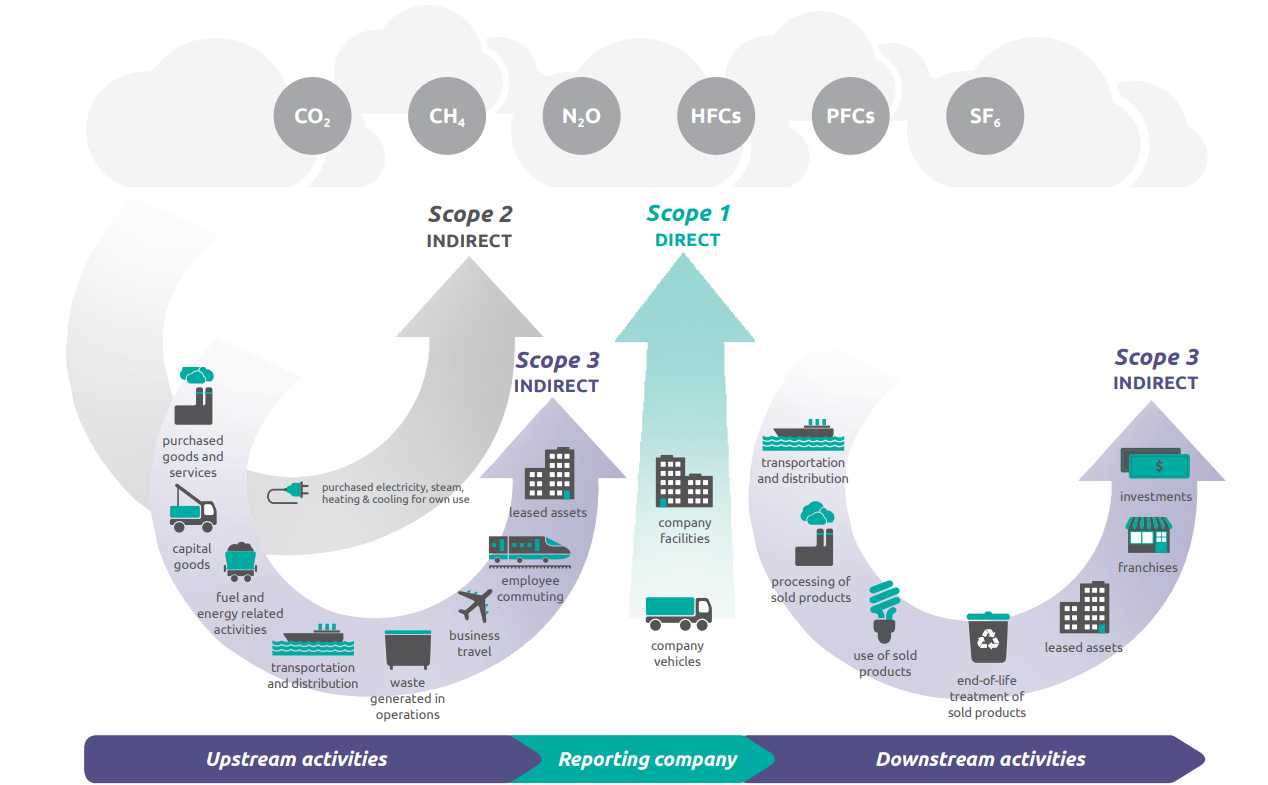

When it comes to measuring a company’s carbon footprint, Scope 3 emissions are often the trickiest and the biggest piece of the puzzle.

Unlike Scope 1 (direct emissions) and Scope 2 (indirect emissions from energy use), Scope 3 includes all the other emissions a company is indirectly responsible for, up and down its value chain. That means emissions from everything the company buys, how it delivers its products, how employees travel, and even what happens when customers are done with the product.

To make it a bit easier, the Greenhouse Gas Protocol breaks Scope 3 into 15 categories. Here’s a simple breakdown:

Upstream activities (before your product or service is made)

Purchased goods and services

All the emissions from making the stuff your company buys, like raw materials, packaging, or software services. If you run a café, this would be the emissions from growing coffee beans or making the napkins you use.Capital goods

These are the big purchases, like machines, buildings, or vehicles. Emissions come from producing those long-term assets.Fuel- and energy-related activities

Even though Scope 2 covers your electricity use, this category covers emissions from producing and transporting that fuel or energy before it gets to you.Upstream transportation and distribution

Emissions from getting your products to your company, from suppliers to your warehouse or store. This includes trucks, ships, or even planes.Waste generated in operations

Everything you throw away during operations, like office paper, manufacturing scrap, or food waste, has an emissions footprint.Business travel

Flights, trains, rental cars, if your employees travel for work, those emissions count here.Employee commuting

How your employees get to and from work, whether it’s by car, public transport, or bike.Upstream leased assets

If you rent equipment, office space, or vehicles, the emissions from running those assets go here, if they’re not already counted in Scope 1 or 2.

Downstream activities (after your product or service leaves you)

Downstream transportation and distribution

Once your product leaves the warehouse or store and is headed to a customer, those shipping emissions count here.Processing of sold products

If your product is used to make something else, and processing it causes emissions (think: raw steel turned into car parts), that goes in this category.Use of sold products

If your product uses energy when customers use it, like a washing machine or a car, those emissions count here.End-of-life treatment of sold products

What happens when your product is thrown away or recycled? This covers emissions from waste treatment, incineration, or landfill.Downstream leased assets

If you lease out things like vehicles or machinery, the emissions from how your customers use them go here.Franchises

If you operate through franchises (like fast food chains), this includes emissions from those locations not directly owned by you.Investments

For financial institutions, emissions from where they put their money, like investments, loans, or insurance, are counted here.

Tip: Start by setting organizational boundaries (who’s in your reporting), then define operational boundaries (what emissions to track).

3. How to choose an operational boundary?

Keep reading with a 7-day free trial

Subscribe to CSRD Simplified to keep reading this post and get 7 days of free access to the full post archives.