VSME: Simplifying Sustainability Reporting for SMEs

VSME: A Simplified Guide for SMEs Under CSRD

1. Introduction

Sustainability reporting isn’t just for large companies anymore. The Corporate Sustainability Reporting Directive (CSRD) brings new challenges for businesses of all sizes, requiring transparent disclosures about their environmental, social, and governance (ESG) impacts. While large corporations have their European Sustainability Reporting Standards (ESRS) to follow, what about smaller businesses that don’t have the same resources or expertise?

This is where the Voluntary Sustainability Reporting Standard (VSME) comes into the picture. The VSME is a simpler framework designed for Micro, Small, and Medium-sized Enterprises). Let’s break down what the VSME is.

2. What is the VSME?

The VSME standard is a voluntary framework aimed at micro, small, and medium-sized enterprises (SMEs) that want to enhance their sustainability practices and reporting without the complexity of larger frameworks. Its key objectives include:

Streamlining sustainability reporting to meet the demands of larger companies, banks, and investors.

Simplifying access to finance by offering reliable sustainability data to financial institutions.

Encouraging better sustainability management to improve resilience and competitive growth.

Contributing to a sustainable and inclusive economy by making reporting accessible to smaller players.

While SMEs are exempt from the CSRD’s mandatory reporting requirements, the VSME offers them a way to participate voluntarily.

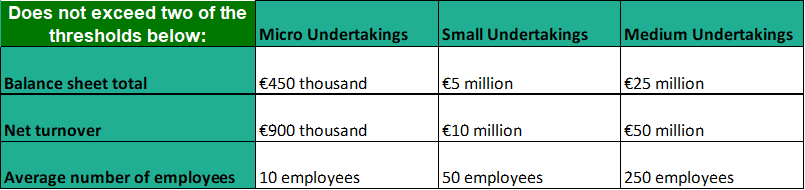

The VSME applies to:

3. How to Report Using the VSME

The VSME is designed to be flexible and easy to use, addressing SMEs’ limited resources and expertise. Reporting under the VSME consists of two modules:

Basic Module: This entry-level module focuses on key disclosures across 11 metrics, covering the minimum information SMEs need to provide.

Comprehensive Module: This optional module expands on the Basic Module with nine additional metrics, catering to the needs of more advanced SMEs or those responding to specific demands from banks, investors, or corporate clients.

SMEs can choose their level of reporting based on their capabilities and stakeholders’ needs. However, once a module is selected, it must be completed in its entirety. While, the ESRS requires a detailed materiality analysis to determine what to report, this is not required for the VSME.

4. Basic Module

The Basic Module serves as the foundation for sustainability reporting, offering a clear and structured approach to disclosing key environmental, social, and governance (ESG) metrics. Here’s a snapshot of its core elements:

What does the Basic Module cover?

General information

Organizations must report their:Reporting scope: Basic Module alone or with Comprehensive Module.

Legal structure, financials (balance sheet size, turnover), and workforce data.

Sustainability certifications, if any.

Environmental metrics

Energy & GHG emissions: Total energy consumption (renewable and non-renewable) and emissions broken down by Scope 1 (direct) and Scope 2 (indirect from purchased energy).

Pollution: Reporting on emissions to air, water, and soil, aligned with existing regulations.

Biodiversity: Impact on sensitive areas (e.g., land use in hectares).

Water use: Total water withdrawal, especially in high-stress areas.

Circular economy: Waste management practices and material flows.

Social metrics

Workforce breakdown by gender, contract type, and location.

Health and safety, including accident rates and fatalities.

Pay equity, training hours, and collective bargaining coverage.

Governance metrics

Instances of corruption or bribery (convictions and fines).

Who should use the Basic Module?

Small and medium-sized enterprises (SMEs) or organizations beginning their sustainability journey. It’s designed to balance clarity and comprehensiveness while keeping reporting manageable.

5. Comprehensive Module

The Comprehensive Module is for organizations seeking to provide detailed insights into their sustainability practices, catering to the needs of investors, banks, and other stakeholders.

What makes it comprehensive?

Strategic insights

Business model and strategy, especially regarding sustainability.

Practices and policies for transitioning to a sustainable economy.

Enhanced environmental metrics

Scope 3 GHG emissions: Indirect emissions from the value chain, e.g., transportation or product use.

GHG reduction targets: Detailed goals for emissions reductions, including specific actions.

Climate risks: Assessment of climate-related hazards and their impact on financial performance.

Expanded social metrics

Female-to-male ratio in management.

Policies addressing human rights, such as child labor and discrimination.

Reporting confirmed incidents of human rights violations and mitigation actions.

Governance focus

Revenues from sensitive sectors (e.g., fossil fuels, controversial weapons).

Gender diversity in governance bodies.

Basic vs. Comprehensive Module

Why choose the Comprehensive Module?

It’s ideal for organizations needing to meet regulatory requirements or providing in-depth data for business partners assessing sustainability risks.

6. Conclusion

The VSME is more than just a scaled-down version of ESRS. It’s a thoughtful framework designed to help SMEs navigate the growing demand for sustainability reporting without overwhelming them. With its modular design, simplified language, and focus on accessibility, the VSME empowers businesses to showcase their sustainability efforts. Whether starting with the Basic Module or advancing to the Comprehensive Module, SMEs now have a practical and flexible tool to meet the growing demands of stakeholders and contribute to a more sustainable economy.

Relevant Sources

EFRAG Cover Letter for the VSME.pdf